The International Atomic Energy Agency (IAEA) defined cogeneration as: the integration of nuclear power plants with other systems and applications.

The heat generated by the nuclear power plants can be used to produce a vast range of products such as cooling, heating, process heat, desalination and hydrogen. The use of nuclear energy for cogeneration provides many economic, environmental and efficiency-related benefits. Cogeneration options may be different; depending on the technology, reactor type, fuel type and temperature level.

Source: IAEA

The use of nuclear energy for cogeneration also provides the benefit of using nuclear fuel in more efficient and eco-friendly manner. Energy and exergy analyses show that the performance of a nuclear power plant may be increased if it is used in a cogeneration mode. The use of nuclear energy for cogeneration applications can also lead to a drastic reduction in the environmental impact. However, integrating nuclear power plant with any other sub-system for cogeneration can greatly be affected by the performance parameters of the nuclear power plant and the site where it is situated.

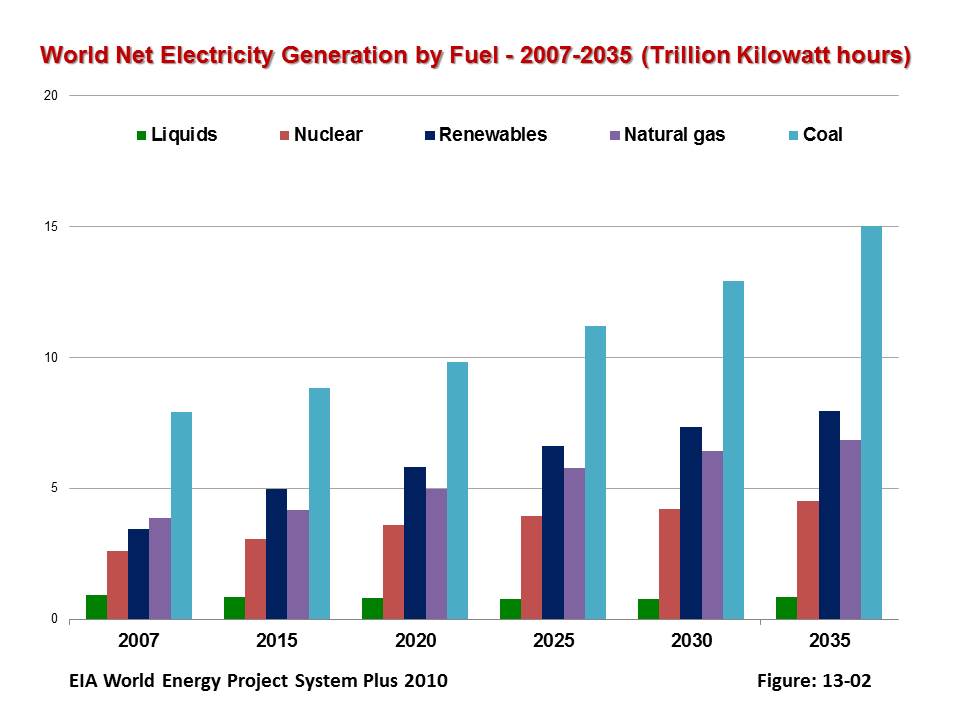

Electricity is at the heart of modern economies and it is providing a rising share of energy services. Demand for electricity is set to increase further as a result of rising household incomes, with the electrification of transport and heat, and growing demand for digital connected devices and air conditioning.

Rising electricity demand was one of the key reasons why global CO2 emissions from the power sector reached a record high in 2018, yet the commercial availability of a diverse suite of low emissions generation technologies also puts electricity at the vanguard of efforts to combat climate change and pollution. Decarbonised electricity, in addition, could provide a platform for reducing CO2 emissions in other sectors through electricity-based fuels such as hydrogen or synthetic liquid fuels. Renewable energy also has a major role to play in providing access to electricity for all.

A report published by IAEA on the subject of World Nuclear Electricity Production, Energy Electricity and Nuclear Power Estimates:

- Total electricity production grew by 3.9 percent in 2018, while the growth in nuclear electricity production was 2.4 percent;

- Among the various sources for electricity production, coal remained dominant despite the significant growth of renewable and natural gas based generation;

- The share of electricity production from natural gas remained at about 23 percent of total electricity production;

- The contribution of hydropower and renewable energy sources continued to increase significantly, reaching 25.8 percent in 2018, while the share of nuclear electricity production remained at about 10.2 percent of the total electricity production;

- Electricity generation from operational nuclear reactors increased about 2.4 percent in 2018, reaching 2563 TW∙h.; and

- Nuclear power accounted for about 10 percent of total electricity production in 2018.

Nuclear reactors generated a total of 2563 TWh of electricity in 2018, up from 2502 TWh in 2017. This is the sixth successive year that nuclear generation has risen, with output 217 TWh higher than in 2012:

![]()

In 2018 the peak total net capacity of nuclear power in operation reached 402 GWe, up from 394 GWe in 2017. The end of year capacity for 2018 was 397 GWe, up from 393 GWe in 2017.

Usually only a small fraction of operable nuclear capacity does not generate electricity in a calendar year. However, since 2011, the majority of the Japanese reactor fleet has been awaiting restart. Four Japanese reactors were restarted in 2018, joining the five reactors that had restarted in previous years:

![]()

Energy and Electricity Projections:

- World energy consumption is expected to increase by 16 percent by 2030 and by 38 percent by 2050, at an annual growth rate of about 1 percent;

- Electricity consumption will grow at a higher rate of about 2.2 percent per year up to 2030 and around 2 percent per year thereafter; and

- The share of electricity in total final energy consumption will thus increase from 18.8 percent in 2018 to 21 percent by 2030 and to 26 percent by the middle of the century.

In addition to generating electricity, nuclear reactors can provide heat for multiple uses including heating homes as well as commercial and industrial buildings in a safe manner and with minimum environmental impacts.

Nuclear Process Heat for Industry. Nuclear energy is an excellent source of process heat for various industrial applications including desalination, synthetic and unconventional oil production, oil refining, biomass-based ethanol production, and in the future: hydrogen production.

According to the World Nuclear Association (Updated April 2020):

- For most major industrial heat applications, nuclear energy is the only credible non-carbon option.

- Light water reactors produce heat at relatively low temperatures in relation to many industrial needs, hence the technology focus has been on high-temperature gas-cooled reactors (HTR) and more recently on molten salt reactors (MSR) producing heat at over 700°C; and

- In 2019 there were 79 nuclear reactors used for desalination, district heating, or process heat, with 750 reactor-years of experience in these, mostly in Russia and Ukraine.

In general, heat consumption can be divided into the following two temperature levels:

- Low-temperature heat, which includes hot water or low-quality steam for district heat, desalination, and other purposes; and

- High-temperature process heat that includes process steam for various industrial applications (aluminum production, chemicals) or high temperature heat for conversion of fossil fuels, hydrogen production, and so on.

The direct use of nuclear heat in homes and industries is nothing new. There are, however, substantial differences between the properties and applications of electricity and of heat, as well as between the markets for these different forms of energy. These differences as well as the intrinsic characteristics of nuclear reactors are the reasons why nuclear power has predominantly penetrated the electricity market and had relatively minor applications as a direct heat source.

When the first nuclear power reactor at Calder Hall in the United Kingdom came into commercial operation in October 1956, it provided electricity to the grid and heat to a neighbouring fuel reprocessing plant. After more than 40 years, the four 50 megawatt-electric (MWe) Calder Hall units are still in operation. In Sweden, the Agesta reactor provided hot water for district heating to a suburb of Stockholm for a decade, starting in 1963.

Since these early days of nuclear power development, the direct use of heat generated in reactors has been expanding. Countries such as Bulgaria, Canada, China, the Czech Republic, Germany, Hungary, India, Japan, Kazakstan, Russia, Slovakia, Sweden, Switzerland, and Ukraine have found it convenient to apply nuclear heat for district heating or for industrial processes, or for both, in addition to electricity generation. Though less than 1 percent of the heat generated in nuclear reactors worldwide is at present used for district and process heating, there are signs of increasing interest in these applications.

About 33 percent of the world’s total energy consumption is currently used for electricity generation. This share is steadily increasing and is expected to reach 40 percent by the year 2015. Of the rest, heat consumed for residential and industrial purposes and the transport sector constitute the major components, with the residential and industrial sectors having a somewhat larger share. Practically the entire heat market is supplied by burning coal, oil, gas, or wood. Overall energy consumption is steadily increasing and this trend is expected to continue well into the next century. Conservation and efficiency improvement measures have in general reduced the rate of increase of energy consumption, but their effect is not large enough to stabilize consumption at current values.

It is important to understand that the transportation of heat is difficult and relatively expensive. The need for a pipeline, thermal isolation, pumping, and the corresponding investments, heat losses, maintenance, and pumping energy requirements make it impractical to transport heat beyond distances of a few kilometers or, at most, some tens of kilometers. There is also a strong size effect. The specific costs of transporting heat increase sharply as the amount of heat to be transported diminishes. Compared to heat, the transport of electricity from where it is generated to the end-user is easy and cheap, even to large distances measured in hundreds of kilometers.

All industrial users who require heat also consume electricity. The proportions vary according to the type of process, where either heat or electricity might have a predominant role. The demand for electricity can be supplied either from an electrical grid, or by a dedicated electricity generating plant. Co-generating electricity and heat is an attractive option. It increases overall energy efficiency and provides corresponding economic benefits. Co-generation plants, when forming part of large industrial complexes, can be readily integrated into an electrical grid system to which they supply any surplus electricity generated. In turn, they would serve as a backup for assurance of electricity supply. Such arrangements are often found to be desirable.

From the technical point of view, nuclear reactors are heat-generating devices. There is plenty of experience of using nuclear heat in both district heating and in industrial processes, so the technical aspects can be considered well proven. There are no technical impediments to the application of nuclear reactors as heat sources for district or process heating. In principle, any type and size of nuclear reactor can be used for these purposes. Potential radioactive contamination of the district heating networks or of the products obtained by the industrial processes is avoided by appropriate measures, such as intermediate heat exchanger circuits with pressure gradients which act as effective barriers. No incident involving radioactive contamination has ever been reported for any of the reactors used for these purposes.

The residential and the industrial sectors constitute the two major components of the overall heat market. Within the residential sector, while heat for cooking has to be produced directly where it is used, the demand for space heating can be and is often supplied from a reasonable distance by a centralized heating system through a district heating transmission and distribution network serving a relatively large number of customers.

Here are two major applications:

1. District Heating:

District heating is a system for distributing heat generated in a centralized location for residential and commercial heating requirements such as space heating and water heating. District heating networks generally have installed capacities in the range of 600 to 1200 megawatt-thermal (MWth) in large cities, decreasing to approximately 10 to 50 MWth in towns and small communities.

Exceptionally, capacities of 3000 to 4000 MWth can be found. Obviously, a potential market for district heating only appears in climatic zones with relatively long and cold winters. In western Europe, for example, Finland, Sweden, and Denmark are countries where district heating is widely used, and this approach is also applied in Austria, Belgium, Germany, France, Italy, Switzerland, Norway, and the Netherlands, though to a much lesser degree. The annual load factors of district heating systems depend on the length of the cold season when space heating is required, and can reach up to about 50 percent, which is still way below what is needed for base load operation of plants.

In addition, to assure a reliable supply of heat to the residences served by the district heating network, adequate back-up heat generating capacity must be provided. This implies the need for redundancy and generating unit sizes corresponding to only a fraction of the overall peak load. The temperature range required by district heating systems is around 100 to 150° C. In general, the district heating market is expected to expand substantially. Not only because it can compete economically in densely populated areas with individual heating arrangements, but also because it offers the possibility of reducing air pollution in urban areas. While emissions resulting from the burning of fuel can be controlled and reduced up to a point in relatively large centralized plants, this is not practical in small individual heating installations fuelled by gas, oil, coal, or wood.

In addition, to assure a reliable supply of heat to the residences served by the district heating network, adequate back-up heat generating capacity must be provided. This implies the need for redundancy and generating unit sizes corresponding to only a fraction of the overall peak load. The temperature range required by district heating systems is around 100 to 150° C. In general, the district heating market is expected to expand substantially. Not only because it can compete economically in densely populated areas with individual heating arrangements, but also because it offers the possibility of reducing air pollution in urban areas. While emissions resulting from the burning of fuel can be controlled and reduced up to a point in relatively large centralized plants, this is not practical in small individual heating installations fuelled by gas, oil, coal, or wood.

For the district heating market, co-generation nuclear power plants are one of the supply options. In the case of medium to large nuclear reactors, due to the limited power requirements of the heat market and the relatively low load factors, electricity would be the main product, with district heating accounting for only a small fraction of the overall energy produced. These reactors, including their sitting, would be optimized for the conditions pertaining to the electricity market, district-heating being, in practice, a by-product. Should such power plants be located close enough to population centers in cold climatic regions, they could also serve district heating needs. This has been done in Russia, Ukraine, the Czech Republic, Slovakia, Hungary, Bulgaria, and Switzerland, using up to about 100 MWth per power station. Similar applications can be expected for the future wherever similar boundary conditions exist.

For small co-generation reactors corresponding to power ranges of up to 300 MWe and 150 MWe, respectively, the share of heat energy for district heating would be larger. Nevertheless, electricity would still be expected to constitute the main product, assuming base-load operation, for economic reasons. The field of application of these reactors would be similar to the case of medium or large co-generation reactors. Additionally, however, they could also address specific objectives, such as the energy supply of concentrated loads in remote and cold regions of the world.

Heat-only reactors for district heating are another option. Such applications have been implemented on a very small scale (a few MWth) as experimental or demonstration projects. Construction of two units of 500 MWth was initiated in Russia in 1983-85, but later interrupted. There are several designs being pursued, and it is planned to start construction of a 200 MWth unit soon in China. Clearly, the potential applications of heat-only reactors for district heating are limited to reactors in the very small size range. These reactors are designed for sitting within or very close to population centers so that heat transmission costs can be minimal. Even so, economic competitiveness is difficult to achieve due to the relatively low load factors required, except in certain remote locations where fossil fuel costs are very high and the winter is very cold and long.

In summary, the prospects for nuclear district heating are real, but limited to applications where specific conditions pertaining to both the district heating market and to the nuclear reactors can effectively be met. The prospects for co-generation reactors, especially in the SMR range, seem better than for heat-only reactors, mainly because of economic reasons.

2. Industrial Processes:

Within the industrial sector, process heat is used for a very large variety of applications with different heat requirements and with temperature ranges covering a wide spectrum. While in energy intensive industries the energy input represents a considerable fraction of the final product cost, in most other processes it contributes only a few percent. Nevertheless, the supply of energy has an essential character. Without energy, production would stop. This means that a common feature of practically all industrial users is the need for assurance of energy supply with a very high degree of reliability and availability, approaching 100 percent in particular for large industrial installations and energy intensive processes.

Regarding the power ranges of the heat sources required, similar patterns are found in most industrialized countries. In general, about half of the users require less than 10 MWth and another 40 percent between 10 and 50 MWth. There is a steady decrease in the number of users as the power requirements become higher. About 99 percent of the users are included in the 1 to 300 MWth ranges, which accounts for about 80 percent of the total energy consumed. Individual large users with energy intensive industrial processes cover the remaining portion of the industrial heat market with requirements up to 1000 MWth, and exceptionally even more. This shows the highly fragmented nature of the industrial heat market.

The possibility of large-scale introduction of heat distribution systems supplied from a centralized heat source, which would serve several users concentrated in so-called industrial parks — seems rather remote at present, but could be the trend on a long term. Contrary to district heating, the load factors of industrial users do not depend on climatic conditions. The demands of large industrial users usually have base load characteristics.

The temperature requirements depend on the type of industry, covering a wide range up to around 1500° C. The upper range above 1000° C is dominated by the iron/steel industry. The lower range up to about 200 to 300° C includes industries such as seawater desalination, pulp and paper, or textiles. Chemical industry, oil refining, oil shale and sand processing, and coal gasification are examples of industries with temperature requirements of up to the 500 to 600° C level. Non-ferrous metals, refinement of coal and lignite, and hydrogen production by water splitting are among applications that require temperatures between 600 and 1000° C.

The characteristics of the market for process heat are quite different from district heating, though there are some common features, particularly regarding the need for minimal heat transport distance. Industrial process heat users, however, do not have to be located within highly populated areas, which by definition constitute the district heating market. Many of the process heat users; in particular, the large ones, can be and usually are located outside urban areas, often at considerable distances. This makes joint sitting of nuclear reactors and industrial users of process heat not only viable, but also desirable in order to drastically reduce or even eliminate the heat transport costs.

For large size reactors, the usual approach is to build multiple unit stations. When used in the co-generation mode, electricity would always constitute the main product. Such plants, therefore, have to be integrated into the electrical grid system and optimized for electricity production. For reactors in the SMR size range, and in particular for small and very small reactors, the share of process heat generation would be larger, and heat could even be the predominant product. This would affect the plant optimization criteria, and could present much more attractive conditions to the potential process heat user. Consequently, the prospects of SMRs as co-generation plants supplying electricity and process heat are considerably better than those of large reactors.

Several co-generation nuclear power plants in operation already supply process heat to industrial users. The largest projects implemented are in Canada (Bruce, heavy-water production and other industrial/agricultural users) and in Kazakstan (Aktau, desalination). Other power reactors that currently produce only electricity could be converted to co-generation. Should there be a large process heat user close to the plant interested in receiving this product; the corresponding conversion to co-generation would be technically feasible. It would, however, involve additional costs, which would have to be justified by a cost/benefit analysis. Some such conversion projects could be implemented but, in general, prospects for this option seem rather low.

Installing a new nuclear co-generation plant close to an existing and interested industrial user has better prospects. Even better would be a joint project whereby both the nuclear co-generation plant and the industrial installation requiring process heat are planned, designed, built, and finally operated together as an integrated complex.

Current and advanced light or heavy-water reactors offer heat in the low temperature range, which corresponds to the requirements of several industrial processes. Among these, seawater desalination is presently seen as the most attractive application. Other types of reactors, such as liquid metal-cooled fast reactors and high temperature gas-cooled reactors can also offer low temperature process heat, but in addition, they can cover higher temperature ranges. This extends their potential field of application. These reactors still require substantial development in order to achieve commercial maturity. Should they achieve economic competitiveness as expected, their prospects seem to be promising in the medium to long term, especially for high temperature industrial applications.

Heat-only reactors have not yet been applied on an industrial/commercial scale for the supply of process heat. Several designs have been developed and some demonstration reactors have been built. Economic competitiveness seems to be an achievable goal according to many studies, which have been performed, but this is something yet to be proven in practice. The potential market for such heat-only reactors would be limited to the very small size range, i.e. below about 500 MWth.

The prospects for applying nuclear energy to district and process heating are closely tied to the prospects of deploying SMRs. A recent market assessment for SMRs found that 70 to 80 new units are planned in about 30 countries up to the year 2015. It was also found that about a third of these units are expected to be applied specifically to nuclear desalination. Of the rest, a substantial share could very well supply heat in addition to electric energy, while a few are expected to be heat-only reactors.

Resources:

- US Energy Information Administration: Independent Statistics and Analysis;

- IAEA: Nuclear Technology Outlook Review 2010;

- World Nuclear Association: World Energy Needs and Nuclear Power;

- US Energy Information Administration: International Energy Outlook 2010; and

- IAEA Bulletin: Nuclear Power Applications – Supply of heat for homes and industries.

- This chapter was published on “Inuitech – Intuitech Technologies for Sustainability”

on January 15, 2012; and - This chapter was updated on 14 June 2020