This article was published on June 2011 when Dr. Ali was at the Oxford University

1. Nuclear Energy:

In spite of abundant UK renewable resource, as regards wind; marine; and solar, the current share of renewables in the UK energy mix represents only 3 percent whereas the share of nuclear energy for decarbonizing electricity generation in the UK jumped to almost 18 percent in 2009 from 13 percent in 2008. According to the World Nuclear Association, the total electricity supply was 5 percent lower than the previous year as a result of the global economic crisis. Domestic nuclear production was some 25 percent greater than for 2008 due to improved plant availability.

Here are some realities to appreciate the status of nuclear energy in the UK:

- In 2009, electricity from nuclear power plants produced just over 69 billion kWh net, or 18 percent of total electricity supply from all sources (371 billion kWh net). Gas-fired generation accounted for 44 percent of total (165 billion kWh); coal-fired 28 percent (104 billion kWh); wind 2.5 percent (9.3 billion kWh); hydro 1.3 percent (5.2 billion kWh); and other renewables 3 percent (11.5 billion kWh, mainly from biomass);

- In 2009, net electricity imports from France – mostly nuclear – 2.8 billion kWh, less than 1 percent of overall supply, compared with 12.5 billion kWh in 2008, or 3.7 percent of final electricity consumption. Per capita electricity consumption was 5220 kWh; and

- In 2009, half of British gas was supplied from imports (compared with 32 percent in 2007), and this is expected to increase to at least 75 percent by 2015, as domestic reserves are depleted. This has major implications for electricity generation, with the amount expected to be from gas to almost double from the 170 billion kWh in 2008.

Electricity generated from nuclear power currently displaces around 14 million tonnes of carbon (MtC) per year, with a range of 7.95 MtC to 19.9 MtC (Depending on whether it is, assumed to displace coal or gasfired electricity generation). This is equivalent to around 9 percent of total UK carbon dioxide (CO2) emissions in 2004 (with a range of 5-12.6 percent).

According to the World Nuclear Association, as of December 2009, here is the status of the UK nuclear energy:

- Generated Electricity 52.5 Billion KWh which represents 13.5 percent (2008);

- 19 Nuclear Reactors were operated and generated electricity 11,035 MWe (2009) which represents 18 percent;

- Currently, there are no nuclear reactors under construction;

- However, there are 4 nuclear reactors planned with the estimated capacity to generate electricity of 6,600 MWe;

- There are 6 nuclear reactors proposed with the estimated capacity to generate electricity of 9,600 MWe;

- The UK required 2,059 tonnes of uranium in 2009; and

- The last four operating Magnox reactors are due to shut down by the end of 2012, leaving seven twin-unit Advanced Gas-Cooled Reactor (AGR) stations and one Pressurized Water Reactor (PWR).

In the late 1990s, nuclear power plants contributed around 25 percent of total annual electricity generation in the UK, but this has gradually declined as old plants, have been shut down, ageing-related problems affected plant availability together with no political will to invest in new nuclear plants.

As far as the government policy is concerned, the question of new nuclear build was, effectively ruled out until 2006, when a review of energy policy reversed the government’s opposition to new nuclear. Government policy in England and Wales has since been supportive of new nuclear plants, which should be, financed and built by the private sector – internalized waste and decommissioning costs as per the industry norm internationally. To facilitate new nuclear build, the government has begun implementing several measures, in particular:

- Streamlining the planning process;

- Carrying out strategic sitting assessment and strategic environmental assessment processes to identify and assess suitable sites for new nuclear plants;

- Ensuring that the regulators are equipped to pre-license designs for new build proposals (the Generic Design Assessment process);

- Introducing legislation to ensure decommissioning and waste management liabilities will be met from operational revenue; and

- Strengthening the EU Emissions Trading Scheme to build investor confidence in long-term carbon pricing.

As a background, since the government reversed its unfavourable policy towards nuclear in 2006, several utilities have begun planning to build new nuclear plants. The initial concern was that the most promising sites were owned by only two organizations: British Energy – which had recently completed restructuring following its financial collapse in 2002 and the government-owned Nuclear Decommissioning Authority (NDA) – which had recently taken ownership of BNFL’s and the UKAEA’s nuclear sites in order to decommission them. Utilities wishing to build new nuclear plants in the UK therefore had to either acquire British Energy, or its sites; or acquire land from the NDA.

EDF successfully bid for British Energy, completing the £12.5 billion acquisition in January 2009. Later in 2009, Centrica bought a 20 percent stake in British Energy for £2.3 billion. Conditions attached to the acquisition of British Energy included the sale of land at Wylfa, Bradwell and either Dungeness or Heysham, as well as to relinquish one of the three grid connection agreements it held for Hinkley Point. Present plans are for four EPR nuclear reactors to be built by EDF Energy at Sizewell in Suffolk and Hinkley Point in Somerset. Planning applications for the first units expected in mid-2011 when the Generic Design Assessment (GDA) process on reactor designs is due to finish. EDF plans to start up the first new reactor (at Hinkley Point) by the end of 2017 and have it grid-connected early in 2018.

Early in 2009, a 50:50 new-build joint venture of RWE npower with E.ON UK was established, now known as Horizon Nuclear Power. A second joint venture of Iberdrola (which owns Scottish Power) with GDF Suez along with Scottish & Southern Energy followed, now known as NuGeneration. This is owned 37.5 percent each by Iberdrola and GDF Suez, and 25 percent by Scottish & Southern. These two partnerships both bid for NDA land alongside old Magnox plants at Oldbury, Wylfa and Bradwell. Other bidders included EDF Energy and Vattenfall. The winning bids for Oldbury and Wylfa were from Horizon Energy that for Bradwell was from EDF. The auction raised £387 million for the NDA. In October 2009, NuGeneration bought a 190 ha site on the north side of Sellafield from the NDA for £70 million, and announced its intention to build up to 3600 MWe of nuclear plant there, with construction beginning around 2015.

2. Low-Carbon Economy:

It is no secret that, electricity use is growing worldwide, providing a range of energy services: lighting, heating and cooling, specific industrial uses, entertainment, information technologies, and mobility. Because its generation remains largely based on fossil fuels, electricity is also the largest and the fastest-growing source of energy-related CO2 emissions, the primary cause of human-induced climate change. Forecasts from the International Energy Agency (IEA) and others show that “decarbonizing” electricity and enhancing end-use efficiency can make major contributions to the fight against climate change. Global and regional trends on electricity supply and demand indicate the magnitude of the decarbonisation challenge ahead.

The efforts associated with the decarbonisation of electricity is leading the world to a low-carbon economy and the fundamental shift in the global economy is the manifestation of the move that the world is making to a low carbon future by investing heavily into the climate change initiatives. These trends are expected to be continued and consequently, the global market for low carbon goods and services is, estimated to grow over £4.3 trillion by 2015. This transition undoubtedly will continue to have a direct impact on the global civilizations, cultures, and humanity, altering the way people live; work; and socialize. There is a huge recognition for the fact that the most important areas of opportunity for the UK’s future economic growth, is the low carbon sector that will create an enormous demand for sustainable technologies, goods, and services. It will play an important role in empowering the country not only to meet its climate change goals but it will also help prosper its societies.

However, toweverhe transition towards a low-carbon economy is needed rapidly. A wide range of technologies including nuclear energy will be essential to achieve stable economic growth, energy security and environmental sustainability by 2050. Annual investments in low-carbon energy technologies averaged approximately USD 165 billion over the last three years. To ensure the energy future IEA analysis suggests that investments in clean technologies will need to reach approximately USD 750 billion, per year by 2030, rising to over USD 1.6 trillion per year from 2030 to 2050.

It is expected by the middle of the next decade over a million people in the UK could be employed in the low-carbon and green manufacturing sectors. It is also anticipated that the UK’s sound regulatory framework will make it a leading destination for green investments which coupled with a tradition of innovation, world leading universities and a skilled workforce gives it the potential to lead the world as a low carbon economy.

3. The Climate Change Act 2008:

The world was astounded with the enactment of the Climate Change Act 2008. The UK has passed legislation that introduced the world’s first long term legally binding framework to tackle the dangers of climate change. The Climate Change Bill was, introduced into Parliament on 14 November 2007 and became law on 26th November 2008.

The UK Government is committed to addressing both the causes and consequences of climate change. The Act creates a new approach to managing and responding to climate change in the UK through: Setting ambitious targets, assuming powers to help achieve them, strengthening the institutional framework, enhancing the UK’s ability to adapt to the impact of climate change and establishing clear and regular accountability to the UK, Parliament and devolved legislatures. As the largest public sector emitter of Carbon emissions, the NHS has a duty to respond to meet the new targets that are now entrenched in law.

The UK Government is committed to addressing both the causes and consequences of climate change. The Act creates a new approach to managing and responding to climate change in the UK through: Setting ambitious targets, assuming powers to help achieve them, strengthening the institutional framework, enhancing the UK’s ability to adapt to the impact of climate change and establishing clear and regular accountability to the UK, Parliament and devolved legislatures. As the largest public sector emitter of Carbon emissions, the NHS has a duty to respond to meet the new targets that are now entrenched in law.

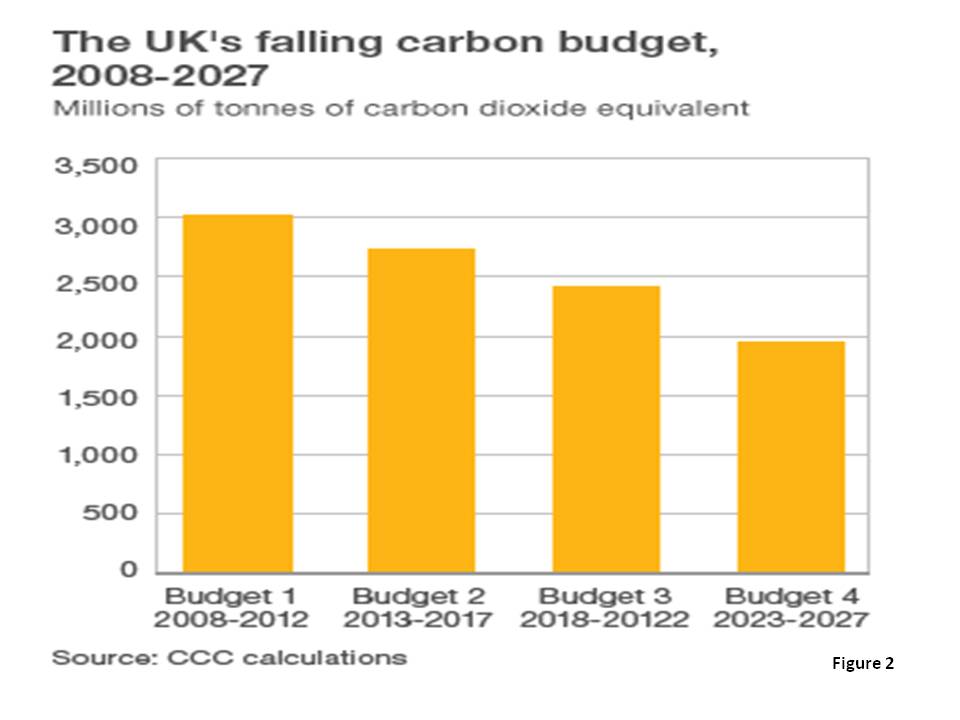

The Act sets targets to reduce CO2 emissions in the UK by 34 percent by 2020 and at least 80 percent on 1990 levels by 2050. This Act also requires the government to set carbon budgets – limits on emissions – for consecutive five-year, mapping out the stages the UK should go through on the way to its long-term goal of cutting CO2 emissions, following what advisors consider the most economic route.

One of the provisions of the Act requires the establishment of the Committee on Climate Change (CCC), a new independent, expert body to advise Government on the level of carbon budgets and where cost effective savings could be made. The Committee will submit annual reports to Parliament on the UK’s progress towards targets and budgets to which the Government must respond, thereby ensuring transparency and accountability on an annual basis.

One of the provisions of the Act requires the establishment of the Committee on Climate Change (CCC), a new independent, expert body to advise Government on the level of carbon budgets and where cost effective savings could be made. The Committee will submit annual reports to Parliament on the UK’s progress towards targets and budgets to which the Government must respond, thereby ensuring transparency and accountability on an annual basis.

These carbon budgets must be set at least three budget periods (2008-2012, 2013-2017, and 2018-2022) in advance, and the fourth carbon budget – the limit on emissions from 2023 to 2027 – has to be set in law by June 2011. The 2027 targets follow recommendations from the CCC.

Two key aims underpinning the Act:

- Improve carbon management and help the transition towards a low carbon economy in the UK; and

- Demonstrate strong UK leadership internationally, signalling that the UK is committed to taking it’s share of responsibility for reducing global emissions in the context of developing negotiations on a post-2012 global agreement at Copenhagen in 2009.

Mr. Huhne, Energy Secretary, noted recently that he agreed with the committee that net CO2 emissions over this period should not exceed 1,950 million tonnes of carbon dioxide equivalent – a 50 percent reduction from 1990 levels. He further noted that:

- “We will aim to reduce emissions domestically as far as is practicable and affordable, but we also intend to keep our carbon trading options open to maintain maximum flexibility and minimize costs in the medium term. Given the uncertainty of looking so far ahead, this is a pragmatic approach.”

The business communities in the UK largely welcomed the UK model articulated to meet the CO2 emission reduction targets and some business groups applauded the adoption of the budget for giving “Greater certainty for business to invest in green technologies”. Besides:

- Many other countries maintained that they too want to see their emissions coming down; so are any of them looking to adopt the UK model;

- Last December, Ireland published a draft climate change bill that bears many of the UK hallmarks;

- Hungary, Finland and Germany have also discussed establishing similar laws in their countries; and

- Beyond that, UK delegations have presented the idea to more than 20 countries spanning the developed world and the developing, on continents from North America to Asia.

The legally binding targets for emissions reductions set out in the Climate Change Act have put nuclear at the centre of national energy strategy. In July 2009, the government set out its policy on nuclear power in a document titled The Road to 2010: Addressing the nuclear question in the twenty first century. It states that nuclear power is “An essential part of any global solution to the related and serious challenges of climate change and energy security.” Furthermore, the document continues: “Nuclear energy is therefore vital to the challenges of sustaining global growth, and tackling poverty.”

4. The Renewable Energy Review:

The CCC was commissioned in May 2010 by the government to conduct a review of renewable energy and advice on the scope to increase ambition for energy from renewable sources. This has important implications for the sector investment climate and Government policy. In September 2010, the committee summarized the analysis of 2020 renewable energy ambition argued that the

Government’s 2020 ambition is appropriate, and there is no need for increase. Instead, the focus should be on ensuring that the existing targets are met: This requires large-scale investment over the next 10 years, supported by appropriate incentives.

The report presented in May 2011 was, based on the following activities:

- Conducted new analysis of technical feasibility and economic viability of renewable and other low-carbon energy technologies;

- Presented scenarios for renewable energy development to 2030 and beyond, and assessed whether it is appropriate now to commit to increased ambition for renewable energy in the 2020s;

- Considered implications of these longer-term scenarios for ambition to 2020; and

- Assessed the key enabling factors for investment in renewable energy technologies, suggesting high-level policy options as appropriate to deliver ambition in 2020 and beyond.

The optimal policy is to pursue a portfolio approach, with each of the different technologies playing a role. In the case of renewable technologies such as offshore wind and marine, this will require the resolution of current uncertainties and the achievement of cost reductions. Therefore, new policies are required to support technology innovation and to address barriers to uptake with the objective to develop suitable renewables as an option for future decarbonisation.

The optimal policy is to pursue a portfolio approach, with each of the different technologies playing a role. In the case of renewable technologies such as offshore wind and marine, this will require the resolution of current uncertainties and the achievement of cost reductions. Therefore, new policies are required to support technology innovation and to address barriers to uptake with the objective to develop suitable renewables as an option for future decarbonisation.

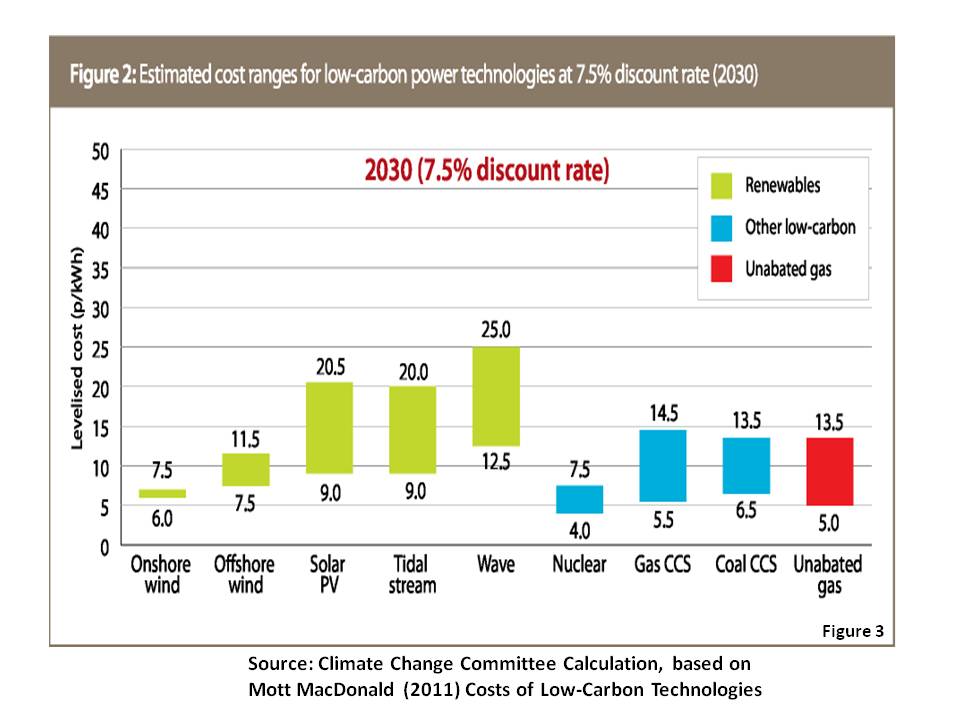

It is likely that a wide range of low-carbon generation technologies

(Renewables and others) will be cheaper than fossil-fired generation (Graph), given a carbon price compatible with overall progress to a low-carbon economy (e.g. around £70 per tonne in 2030):

- Nuclear appears likely to be the lowest-cost low-carbon technology with significant potential for increased deployment; it is likely to be cost competitive with gas CCGT at a £30/tCO2 carbon price in 2020. As such, it should play a major role in decarbonisation, provided that safety concerns are addressed;

- The economics of CCS generation are likely to remain highly uncertain until this technology has been demonstrated at scale;

- Onshore Wind has a comparable cost to nuclear and is therefore also likely to be cost-competitive with gas CCGT by 2020; and

- Most other renewable generation technologies currently appear relatively expensive and are likely to remain so until at least 2020 and in some cases considerably later.

The overall conclusion of the review is that there is scope for significant penetration of renewable energy to 2030 (e.g. up to 45 percent, compared to 3 percent today). Higher levels subsequently (i.e. to 2050) would be technically feasible. Equally however, it would be possible to decarbonise electricity generation with very significant nuclear deployment and have limited renewables; carbon capture and storage may also emerge as a cost-effective technology.

5. Conclusion:

It is true that no energy technology is currently carbon free. Even renewable technologies will lead to fossil fuels being burnt at some point in their construction due to the high levels of fossil fuel usage in almost every transport mode and industrial process, including electricity generation. Coincidently, the CO2 emissions associated with the generation of nuclear electricity are relatively low in comparison with an average value of 4.4 tC/GWh, compared to 243 tC/GWh for coal and 97 tC/GWh for gas. Nevertheless, nuclear and renewables are qualified to be low-carbon technologies.

Here is a simplistic way of looking at the facts articulated in the report:

- The current share of renewables in the UK energy mix represents only 3 percent whereas the nuclear energy share was 18 percent in 2009;

- Full reliance on nuclear would be in appropriate, given uncertainties over costs; site availability; long-term fuel supply and waste disposal; and public acceptability. However, it should play a major role in decarbonisation of electricity mainly because of its cost-competitiveness; and

- There is scope for significant, up to 45 percent, penetration of renewable energy to 2030 and higher levels subsequently to 2050 would be technically feasible. However, it would be fair to assume that full reliance on renewables not only appears to be inappropriate but it would also be immensely expensive.

Perhaps the right answer to this dilemma is the option presented in the report for decarbonising electricity generation in the UK with very significant nuclear deployment and have limited renewables; carbon capture and storage may also emerge as a cost-effective technology. This essentially should recognize nuclear energy as critical to building a low-carbon economy in the UK.

Resources:

- World Nuclear Association – Nuclear Power in the United Kingdom;

- The UK Low Carbon Transition Plan;

- The Renewable Energy Review May 2011;

- The Road to 2010: Addressing the Nuclear Question in the Twenty First Century;

- Investing in a low carbon Britain – Building Britain’s Future;

- IAEA – International Low-Carbon Energy Technology Platform;

- IAEA – Energy Technology Perspective 210 – Scenarios and Strategies;

- Building growth in the Carbon-Economy;

- Summary of the key provisions of the Climate Change Act 2008;

- Ireland aims to pass Climate Change Bill in early 2011; and

- SDC Position Paper: The Role of Nuclear Power in a Low-Carbon Economy.